Bálint Ván, Gábor Lovics, Csaba G. Tóth & Katalin Szőke

Journal of Business Economics – Original Paper – Open access – Published:

Abstract

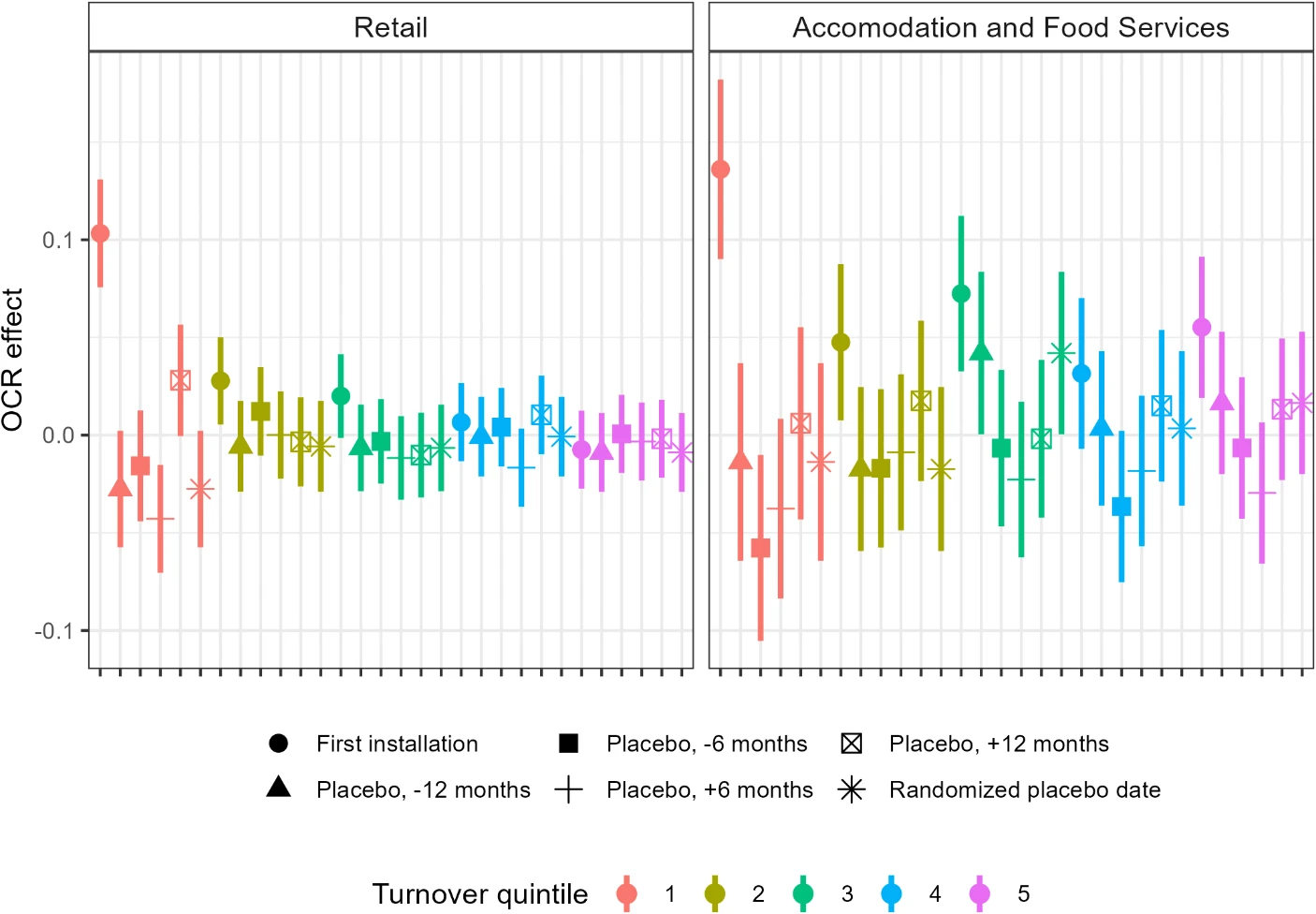

To reduce tax evasion, in 2013 and 2014 the Hungarian government introduced mandatory online cash registers (OCR) in some sectors. As a result, almost 200,000 OCRs have been installed by 100,000 enterprises. We assume that OCR installation does not change the company’s operating model, so the increase in reported turnover around the installation date reflects a reduction in tax evasion. In this paper, we use microdata to estimate the effect of OCR introduction on reported turnover and tax liabilities using fixed-effects panel and event study models.  We identify strong size-related heterogeneity in the retail and the accommodation and food services sectors: smaller companies increased their reported turnover more than larger ones. Since large companies pay the dominant part of value-added tax, the effects on the payment of this tax were mitigated. We find significant spillover effects to suppliers in both sectors, which are slightly stronger among larger companies.

We identify strong size-related heterogeneity in the retail and the accommodation and food services sectors: smaller companies increased their reported turnover more than larger ones. Since large companies pay the dominant part of value-added tax, the effects on the payment of this tax were mitigated. We find significant spillover effects to suppliers in both sectors, which are slightly stronger among larger companies.